The Decree, on the one hand, has intervened by specifying in Article 3 that the collective entrepreneur must adopt an adequate structure not only of organization, but also of administration and accounting. It can be said, in other words, that the need for an accounting, finance and control structure is codified.

In addition, the Decree establishes the purposes of measures and the criteria of arrangements; measures and arrangements, for the purpose of timely detection of business crisis, are understood to be "suitable" and "adequate," respectively, if they enable:

- (i) detect any imbalances of an equity or economic-financial nature, related to the specific characteristics of the enterprise and the business activity carried out by the debtor;

- (ii) verify the sustainability of debts and the prospects for business continuity for at least the next 12 months and detect the signs referred to in paragraph 4 (referred to below); and

- (iii) derive the information necessary to follow the detailed checklist and conduct the practical test for the verification of the reasonable pursuit of recovery, pursuant to the new Article 13(2) CCII.

It should be noted that the second criterion also follows from the new definition of "crisis." In general, the clear purpose emerges that the arrangements intended by the law primarily oblige the company to check the DSCR, noting whether there is excess debt or scarcity of cash flows to service debt.

As a result of the adjustments made by the Decree, pursuant to Article 3(4) CCII, the following constitute signals:

- (a) the existence of payroll debts overdue for at least 30 days equal to more than half of the total monthly payroll amount;

- (b) the existence of payables to suppliers that are at least 90 days past due in an amount exceeding the amount of payables that are not past due;

- (c) the existence of exposures to banks and other financial intermediaries that have been past due for more than 60 days or that have exceeded the limit of credit facilities obtained in any form for at least 60 days, provided that they represent in the aggregate at least 5 percent of the total exposures

- (d) the existence of one or more of the exposures owed to the IRS, INAIL and INPS in the thresholds stipulated in the new Article 25-novies, first paragraph, CCII.

Tags: Sala Noro and Associates

● FAMILY HOLDING: Filippo Sala explains what it is And when to do it...

The choice to create a family holding company is still poorly understood by most entrepreneurs. Yet it is a strategic solution that can play a key role in the life of a family business. It allows its assets to be protected and better managed as it grows and evolves, perhaps by adding new business segments and family members.

The family holding company is an institution that can have an advantageous impact both tax-wise and with a view to proper planning for the generational transition. Indeed, the latter is one of the most insidious obstacles to the future of a family business, as it is often dominated by emotion rather than rationality.

The transfer of ownership and control of assets from one generation to the next involves important cultural, relational and technical issues. Succession is capable of destabilizing established balances, so it requires great foresight, a strategic approach and clear thinking.

The establishment of a family holding company, in addition to providing a more effective management structure, can facilitate the achievement of a common will among several heirs.

❎ WHAT ARE THE BENEFITS AND WHEN TO DO IT

❎ What is a family holding company and what benefits it can offer

A family holding company is a company controlled by members of the same household. Usually, it is a limited liability company model, as it provides greater protection, but it is possible to establish it with any legal form. The choice depends on the context and specific needs.

❎ The main features of a family holding company are very significant from an asset protection and governance point of view:

- the shareholders are members of the family or the same family branch;

- control of the holding company is in the hands of the founding partners (or the founder);

- shareholdings held in the companies belonging to the group contribute to the holding company;

- any family conflicts are handled at the holding company level and are not reflected in the various group companies;

- the holding company has direct and unified control of the subsidiaries, and this ensures stable governance;

- corporate governance choices can be assigned to one or more individuals outside the family;

- through the stipulation of specific clauses in the articles of association, which recognize special rights, and/or shares with multiple or limited voting rights, a specific ownership structure can be guaranteed and certain aspects relating to shareholders and the inclusion of future generations can be regulated.

Thus, placed at the top of a group, the holding company is a legal institution that allows it to carry out a directive and coordinating activity vis-à-vis other companies, whose capital control and shareholding management it holds. As a result, particularly when in the presence of entities belonging to different branches of the family, it ensures a more streamlined operation unencumbered by possible disagreements among shareholders.

Often, the holding company concept is associated only with large multinational corporations. In reality, there is nothing to prevent family-owned SMEs from taking advantage of the many benefits it offers, both in terms of favorable tax treatment and the organization and family governance of assets.

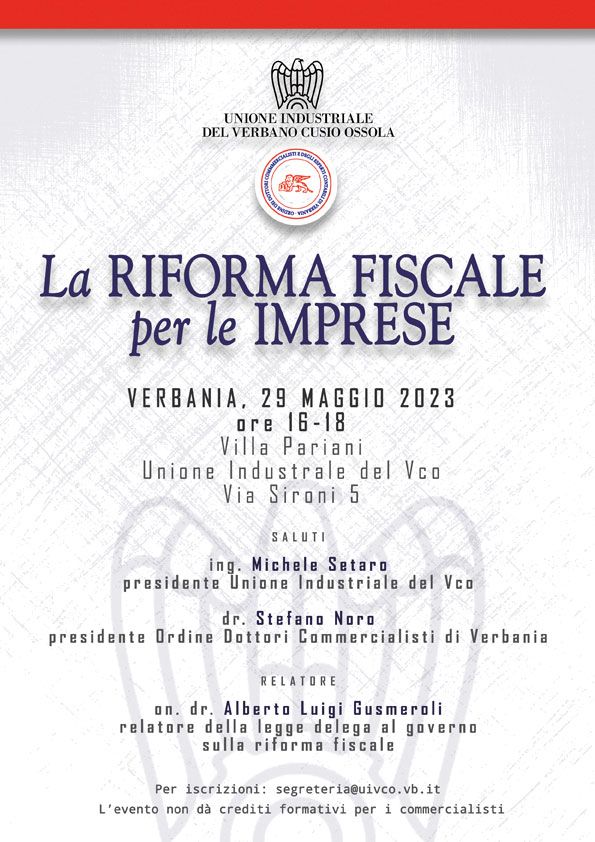

● Tax Reform for Businesses: Introduction by Stefano Noro at the Conference in Verbania speaker Alberto Gusmeroli

A conference entitled "THE TAX REFORM FOR BUSINESSES" was held in Verbania at the headquarters of the Industrial Association with an outstanding speaker Hon. Alberto Gusmeroli, rapporteur of the government's enabling act on tax reform.

The conference was introduced by Engineer Michele Setaro president of the VCO Industrial Association and Dr. Stefano Noro president of the Verbania Association of Accountants.

● Stefano Noro Speaker at the Verbania conference on border crossers: 120 accountants to "lecture" on tax news

President of the Association of Certified Public Accountants of Verbania, Stefano Noro is one of the speakers at the Jan. 20 conference that aims to clarify doubts about the tax treatment of frontier workers in light of current and especially future regulations in view of the new Italy-Switzerland agreements.