The Decree, on the one hand, has intervened by specifying in Article 3 that the collective entrepreneur must adopt an adequate structure not only of organization, but also of administration and accounting. It can be said, in other words, that the need for an accounting, finance and control structure is codified.

In addition, the Decree establishes the purposes of measures and the criteria of arrangements; measures and arrangements, for the purpose of timely detection of business crisis, are understood to be "suitable" and "adequate," respectively, if they enable:

- (i) detect any imbalances of an equity or economic-financial nature, related to the specific characteristics of the enterprise and the business activity carried out by the debtor;

- (ii) verify the sustainability of debts and the prospects for business continuity for at least the next 12 months and detect the signs referred to in paragraph 4 (referred to below); and

- (iii) derive the information necessary to follow the detailed checklist and conduct the practical test for the verification of the reasonable pursuit of recovery, pursuant to the new Article 13(2) CCII.

It should be noted that the second criterion also follows from the new definition of "crisis." In general, the clear purpose emerges that the arrangements intended by the law primarily oblige the company to check the DSCR, noting whether there is excess debt or scarcity of cash flows to service debt.

As a result of the adjustments made by the Decree, pursuant to Article 3(4) CCII, the following constitute signals:

- (a) the existence of payroll debts overdue for at least 30 days equal to more than half of the total monthly payroll amount;

- (b) the existence of payables to suppliers that are at least 90 days past due in an amount exceeding the amount of payables that are not past due;

- (c) the existence of exposures to banks and other financial intermediaries that have been past due for more than 60 days or that have exceeded the limit of credit facilities obtained in any form for at least 60 days, provided that they represent in the aggregate at least 5 percent of the total exposures

- (d) the existence of one or more of the exposures owed to the IRS, INAIL and INPS in the thresholds stipulated in the new Article 25-novies, first paragraph, CCII.

Tags: Stephen Noro

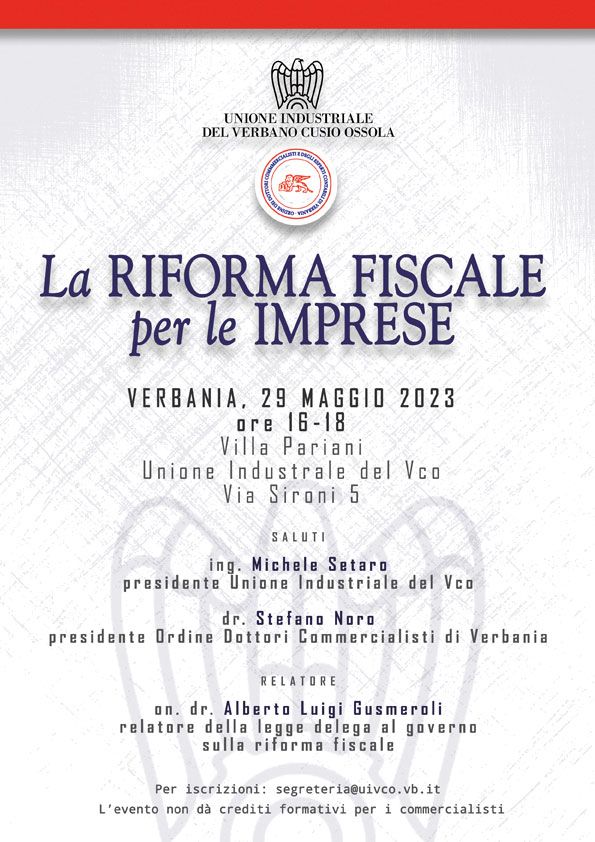

● Tax Reform for Businesses: Introduction by Stefano Noro at the Conference in Verbania speaker Alberto Gusmeroli

A conference entitled "THE TAX REFORM FOR BUSINESSES" was held in Verbania at the headquarters of the Industrial Association with an outstanding speaker Hon. Alberto Gusmeroli, rapporteur of the government's enabling act on tax reform.

The conference was introduced by Engineer Michele Setaro president of the VCO Industrial Association and Dr. Stefano Noro president of the Verbania Association of Accountants.

● Stefano Noro Speaker at the Verbania conference on border crossers: 120 accountants to "lecture" on tax news

President of the Association of Certified Public Accountants of Verbania, Stefano Noro is one of the speakers at the Jan. 20 conference that aims to clarify doubts about the tax treatment of frontier workers in light of current and especially future regulations in view of the new Italy-Switzerland agreements.

● Buying and selling of Oioli by Latteria Soresina: Noro and Associates Hall have managed the operation

Sala Noro and Associates, with a team coordinated by partners Filippo Sala and Stefano Noro, assisted Caseificio F.lli Oioli s.r.l., which specializes in the production of Gorgonzola Dop, in its sale to Latteria Soresina.

Latteria Soresina will have total ownership of the enterprise, but responsibility for running the dairy will be left to the Oioli brothers.

Oioli, which began as a small family business, has developed over the years by bringing Gorgonzola DOP to the domestic and foreign markets, and in 2022 reached a turnover of about 14 million euros, 32 percent more than the previous year.

Latteria Soresina was assisted by KPMG and attorney Giulia Cantini.

The legal aspects of the transaction for Oioli were handled by attorney Giuseppe Melone of the Novara firm Melone Porzio

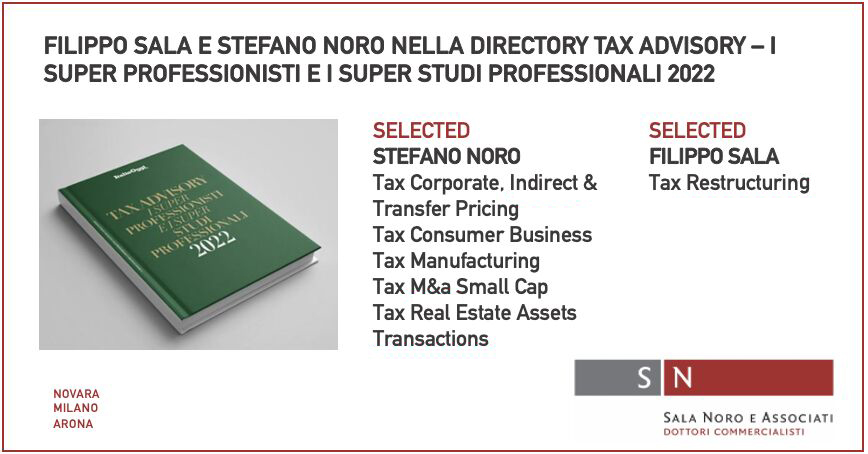

● Tax Advisory: Stefano Noro e Filippo Sala among the super professionals 2022

Stefano Noro and Filippo Sala among Selected professionals in the directory Tax advisory. Super Professionals and Super Firms 2022 published by "ItaliaOggi".